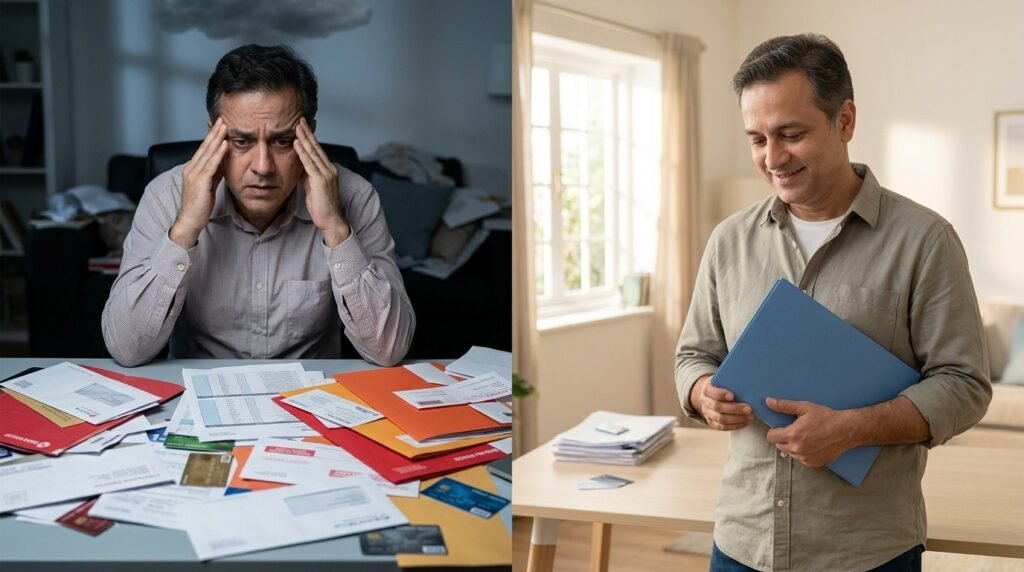

I used to think stress came from work. Deadlines, targets and performance reviews. Then I realised my real manager was not my boss, It was my EMI schedule.

My income was ₹81,000 per month. On paper, that looked respectable but in reality, I was drowning. Personal loan EMI ₹24,000, car loan ₹13,000, credit card EMI ₹9,000 and another small personal loan ₹11,000. Total monthly EMI outflow ₹57,000.

That meant nearly 70% of my income was gone before I bought groceries. At first, LoansJagat personal debt consolidation sounded like just another financial product. But when your mind feels heavier than your wallet, you start looking at solutions differently.

Salary Credited, Peace Debited

The salary notification used to excite me. ₹81,000 credited for about 5 minutes. Then the silent exits began. ₹24,000, ₹13,000, ₹9,000, ₹11,000.

After EMIs, I was left with ₹24,000. Rent ₹15,000, Groceries ₹6,000, Utilities and transport ₹5,000.

Basic expenses alone crossed ₹26,000. That meant I was already ₹2,000 short without even accounting for medical bills, family obligations, or emergencies.

The math was tight, the mind was tighter.

The Brain Does Not Understand EMI Logic

Here is what nobody talks about. Multiple EMIs do not just drain your bank account. They drain your nervous system.

Every 3rd, 5th, 10th, and 18th of the month felt like a mini exam. Different due dates, Different lenders and different interest rates ranging from 13% to 18%.

One missed EMI meant a ₹1,000 late fee plus 2% penal interest. One bounce could damage my credit score.

I started checking my account balance 5 times a day. I calculated expenses while brushing my teeth. I mentally subtracted EMIs while sitting in traffic.

This is what financial anxiety looks like.

When 70% of Income Is Already Spoken For

Financial planners often say your total EMI should not exceed 40% to 50% of your income. I was at 70%.

If your income is ₹81,000 and EMIs are ₹57,000, that leaves only ₹24,000 for survival. Any unexpected expense above ₹5,000 pushes you into borrowing again.

It becomes a cycle. Borrow to pay, pay to survive and survive to borrow again.

I recently read this Reddit post from Ahmedabad where someone earning ₹81,000 confessed they were drowning in EMIs and feeling depressed. Read here: https://www.reddit.com/r/ahmedabad/comments/1quottf/81k_income_but_drowning_in_emis_feeling_depressed/.

Reading it felt uncomfortable because the numbers were similar. The income looked decent, the stress was invisible. The mental load was enormous. It proves that high income does not equal financial peace if obligations are even higher.

The Compound Effect of Chaos

Let us break it down numerically. Suppose total outstanding across loans was ₹12,00,000 at average interest of 15%. With multiple loans, different tenures, and varying rates, I was paying nearly ₹57,000 per month.

Over 5 years, that structure could easily cost ₹17,00,000 to ₹18,00,000 in total repayments. That is ₹5,00,000 to ₹6,00,000 paid in interest.

Now imagine consolidating that ₹12,00,000 into one structured loan at a more competitive blended rate for a longer tenure. The EMI might reduce to around ₹32,000 to ₹35,000 depending on terms.

Old EMI ₹57,000, New EMI approximately ₹34,000 and monthly relief roughly ₹23,000.

That ₹23,000 is not luxury spending money, It is mental oxygen. It allows you to build a ₹1,00,000 emergency fund in 5 months. It reduces your EMI to income ratio from 70% to around 42%. That alone changes your stress level dramatically.

One Loan, One Due Date, One Clear Path

Personal debt consolidation is not about avoiding responsibility. It is about simplifying it.

Instead of 4 lenders, you deal with 1. Instead of 4 interest rates, you have 1. Instead of scattered due dates, you have a single predictable commitment.

LoansJagat personal debt consolidation options are structured for exactly this kind of scenario. The goal is not just lower EMI, It is better cash flow management.

Cash flow clarity equals psychological clarity.

The Financial Rich Solution

A financially strong solution is not just reducing EMI, It is restructuring debt strategically.

Step 1 is consolidating high interest loans into one structured facility.

Step 2 is ensuring EMI stays within 40% to 50% of monthly income.

Step 3 is redirecting surplus cash into an emergency fund and eventually into investments.

For example, if consolidation frees up ₹23,000 monthly, allocating ₹15,000 toward savings and investments at 12% annual return for 10 years could grow to over ₹34 lakh.

That is the difference between surviving debt and reversing it.

Clarity Before Calm

Before restructuring, I felt trapped. After exploring options through the LoansJagat website, the numbers started making sense. Seeing eligibility, comparing rates, and understanding repayment structures in one place removed guesswork.

Clarity does not instantly erase debt, but it immediately reduces mental chaos. And when mental chaos reduces, better financial decisions follow.

Peace Is a Financial Asset

Multiple EMIs do not just reduce income, they reduce sleep, they reduce focus and they reduce confidence.

If 70% of your income is locked into repayments, you are financially overexposed. But there is a structured way out.

Personal debt consolidation is not a shortcut, It is a disciplined reset. Because sometimes the most powerful financial upgrade is not earning more. It is simplifying what you already owe so your mind can finally breathe.

The post The Hidden Mental Stress of Multiple EMIs And How One Loan Can Fix It appeared first on Trade Brains Features.