Welcome to a new week, and a new edition of ‘Open Interest’, where we declutter market trends for you. Flavour of the week: quick commerce. Consumer patterns have changed drastically in favour of the recent crop of ’10-minute delivery’ platforms. But the picture is not entirely rosy.

Q-commerce players continue to struggle with cash burn and elusive profitability, among a long list of hurdles. All the while, wading ahead with their disruption-through-discount mantra. What does the future hold for these new-age players. Jump right in to find out.

Before we begin, you can sign in to our daily and weekly newsletters here.

Narratives change with time as a rule of thumb. However, sometimes they return with vigour. In the business sphere, this is true for the world of quick commerce where the “high cash burn” chatter has returned after the emerging segment shed it off to raise a whopping $28 billion fund raise in the last ten years. In other words, the sector watchers have shifted from “higher growth and high contribution margin” talk to “high cash burn, rising losses, and intense competition”.

It was just a few months ago, when the quick commerce companies were approaching the market to raise equity for easy cash burn in the hope of capturing the evolving market. Investors also valued quick commerce more than food delivery and poured money into these startups that are eyeing the Great Indian Retail Bazaar.

To be fair, it is difficult to predict market dynamics when competition is involved. However, the market was so blinded by the valuations of quick commerce that it overlooked a basic tenet: valuation is not always ‘ceteris paribus’ when it comes to companies that are cash guzzling and loss-making.

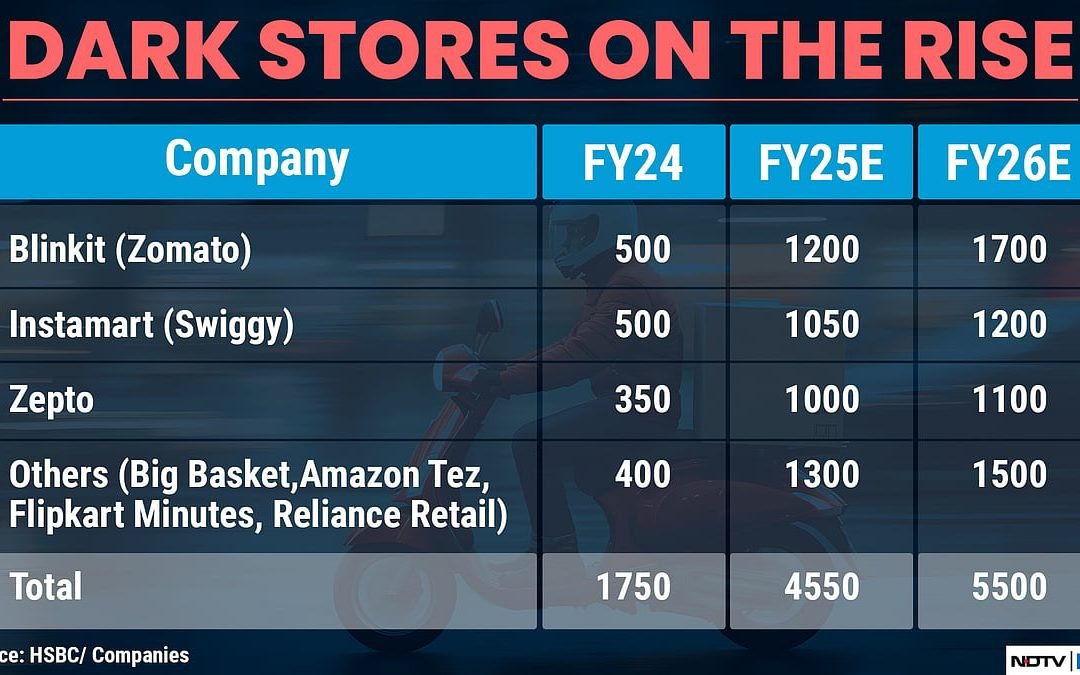

The top quick commerce companies — Blinkit, Instamart, Zepto, Flipkart Minutes, BigBasket, and others — will burn billions of dollars in the next 18–24 months to add feet on the ground and set up dark stores to service these cities.

Nearly 140 cities are covered by quick commerce today, with each company striving to make a mark in the new-age retail space. What’s attracting the investments is the $940 billion opportunity that had earlier lured consumer and modern retailers. Now, it is the turn of quick commerce. India’s quick commerce players accounted for nearly $3.4 billion in revenue in 2024, and this revenue is expected to reach around $10 billion by 2030.

Quick commerce has expanded into almost every segment — from home and personal care, electronics & electrical appliances, apparel & lifestyle, over-the-counter (OTC) medications, and toys, amongst others. This, in turn, has expanded the scope of disruption into other retail formats, including beauty, personal care, electronics, electrical, and childcare platforms.

A recent survey shows that 61% of users now buy most of their beauty or cosmetic products via quick-commerce apps, while 33% use quick commerce only for some purchases and continue buying from their earlier apps. The survey also revealed that half of the surveyed users buy their baby-care supplies and toys from horizontal e-commerce platforms like Amazon or Flipkart, compared to 24% who prefer FirstCry. However, on quick commerce, 55% of surveyed participants indicated they ‘now’ buy most of their kids’ products and supplies on quick-commerce apps, while 24% use quick commerce for some purchases but still buy kids’ products and baby supplies from their earlier apps.

This shift in purchasing preferences is the next round of disruption expected in the coming quarters as quick commerce players expand into tier-2 and tier-3 cities. Furthermore, companies like Zepto are using ‘Saver Packs’ to target high average order value (AOV) by offering higher discounts at the expense of margins. This has led to monthly one-time household spending shifting to these channels as well.

A recent Bank of America research report downgraded food delivery and quick delivery companies, citing cash burn, delayed profitability, shrinking cash balances, and heightened competition.

Break-even for quick commerce players is not on the horizon. Incumbent players are unlikely to relinquish their high-end users who have no loyalty and are only attracted by high teen-digit discounts on basket-level purchases. Companies will respond with higher platform-led discounts, lower delivery charges, and high marketing expenses, which will lead to higher losses in the near term until many of these dark stores scale up or fold up. This business will lead to higher working capital requirement with dark store expansion, high logistics and supply chain costs.

In addition, companies face higher rental expenses, high manpower costs to operate these dark stores, and high marketing spends—all of which are expected to push Ebitda breakeven and real operating cash generation further into the future.

The writing is on the wall: the bleeding will continue for quick commerce companies even as discount seeking unloyal households migrate their monthly purchases to these channels to manage monthly spending and consumer inflation.

Long Live The Consumer!

. Read more on Opinion by NDTV Profit.