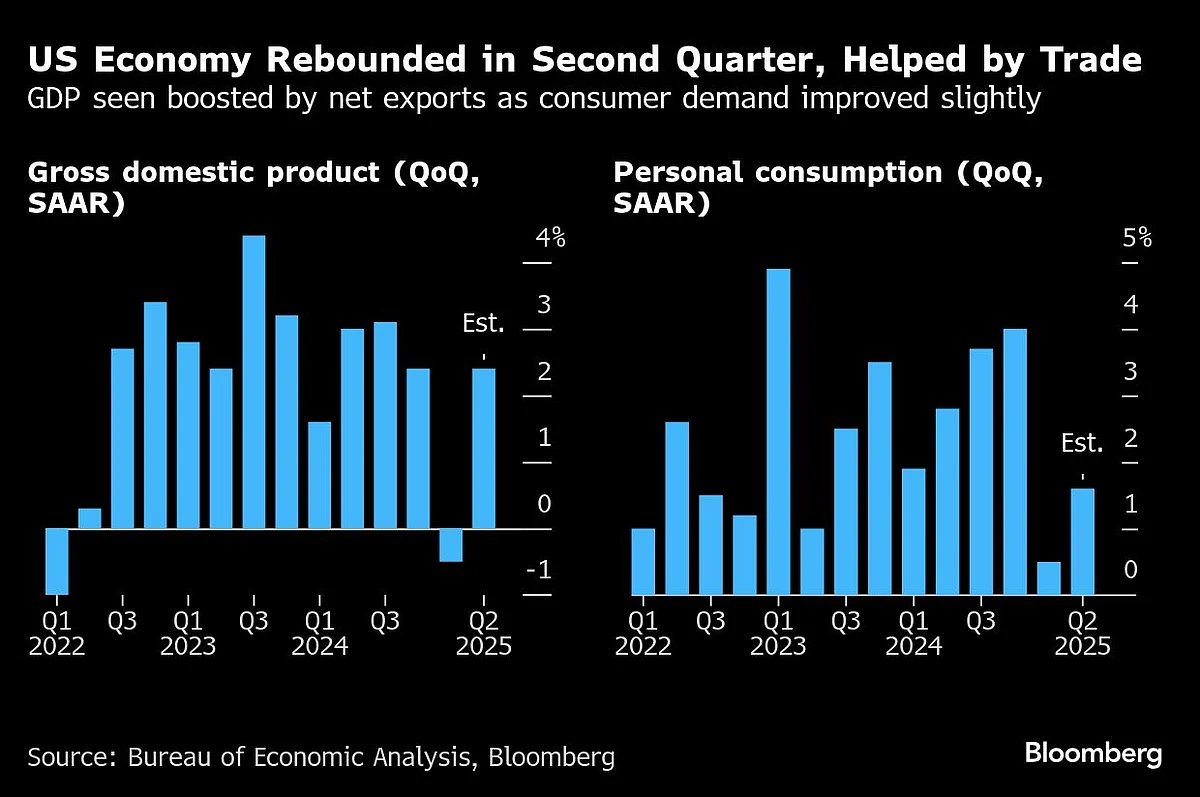

Federal Reserve Chair Jerome Powell and his colleagues will step into the central bank’s board room on Tuesday to deliberate on interest rates at a time of immense political pressure, evolving trade policy, and economic cross-currents.

In a rare occurrence, policymakers will convene in the same week that the government issues reports on gross domestic product, employment and the Fed’s preferred price metrics. Fed officials meet Tuesday and Wednesday, and are widely expected to keep rates unchanged again.

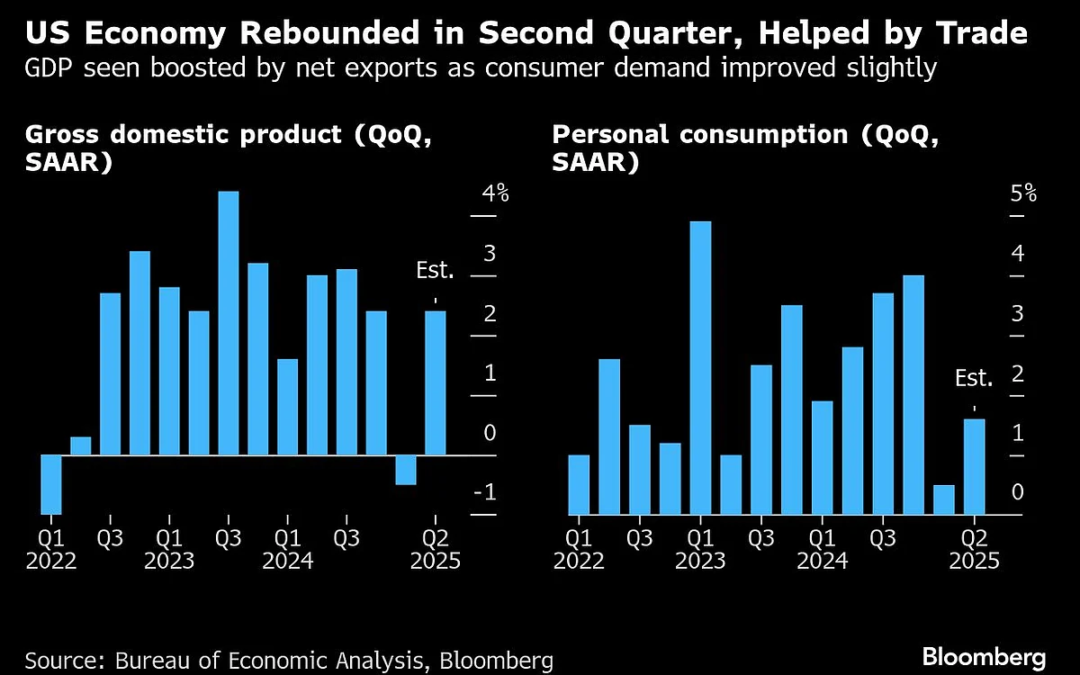

Forecasters anticipate the heavy dose of data will show economic activity rebounded in the second quarter, largely due to a sharp narrowing of the trade deficit, while job growth moderated in July. The third marquee report may show underlying inflation picked up slightly in June from a month earlier.

While the government’s advance estimate of GDP for the quarter is projected to show an annualized 2.4% increase — after the economy shrank 0.5% in January-March — Wednesday’s report will probably reveal only modest household demand and business investment.

The median forecast in a Bloomberg survey calls for a 1.5% gain in consumer spending to mark the weakest back-to-back quarters since the onset of the pandemic in early 2020. A shaky housing market also weighed on second-quarter activity.

At the end of the week, the July jobs report is forecast to show companies are becoming more deliberate in their hiring. Employment likely moderated after a June increase that was boosted by a jump in education payrolls, while the unemployment rate is seen ticking up to 4.2%.

Private payrolls are projected to rise by 100,000 after the smallest advance in eight months. Through the first half of the year, the pace of hiring by companies has eased compared with the 2024 average. The breadth of job growth has been relatively narrow as well. Separate figures out Tuesday are forecast to show job openings declined in June.

A few Fed officials have started to raise concerns about what they see as a fragile job market, including two who’ve said they see merit in considering a rate cut now. Pressure is also mounting from outside the boardroom. President Donald Trump has been vocal about his desire to see Powell & Co. lower borrowing costs for consumers and businesses.

What Bloomberg Economics Says:“We think a consumer-led slowdown poses a risk to the outlook. While June retail sales beat expectations, that was likely a reflection of tariff-driven price increases in certain goods categories. Ultimately, the labor market — which we expect to continue weakening this year — will define the path of consumption.”—Anna Wong, Stuart Paul, Eliza Winger, Estelle Ou & Chris G. Collins, economists. For full analysis, click here

The president has frequently chastised Powell for moving too slowly, while at the same time taking aim at his stewardship over construction cost overruns related to renovation of the Fed’s Eccles Building headquarters in Washington.

Powell and other central bankers have stressed the need for patience as the Trump administration’s tariffs risk a re-acceleration of inflation. So far this year, since a variety of US duties on imports were imposed, price pressures have been modest.

The government’s personal income and spending report for June, due on Friday, is projected to show the Fed’s preferred core inflation gauge accelerated slightly from a month earlier, indicating tariffs are only gradually being passed through to consumers.

-

For more, read Bloomberg Economics’ full Week Ahead for the US

Further north, the Bank of Canada is also set to hold, keeping borrowing costs steady at 2.75% for a third consecutive meeting amid trade uncertainty, sticky core inflation, and an economy that seems to be handling tariffs better than many economists expected. Officials will release a monetary policy report, but it’s not yet known whether they’ll return to point forecasts or release multiple scenarios, as they did in April amid volatile US trade policy.

Industry-based GDP data for May and a flash estimate for June are expected to point to a contraction in the second quarter. Prime Minister Mark Carney is pushing to get a trade deal done with Trump by Aug. 1, but he and the country’s provincial leaders have downplayed expectations, saying they’re focused above all on getting a good agreement.

On a global level, Trump’s Friday deadline also takes center stage, with several countries — including the European Union, South Korea and Switzerland — still hoping to clinch trade agreements.

European Commission chief Ursula von der Leyen will travel to Scotland to meet the US president on Sunday in her attempt to secure a pact. EU officials have repeatedly cautioned that a deal ultimately rests with Trump, making the final outcome difficult to predict.

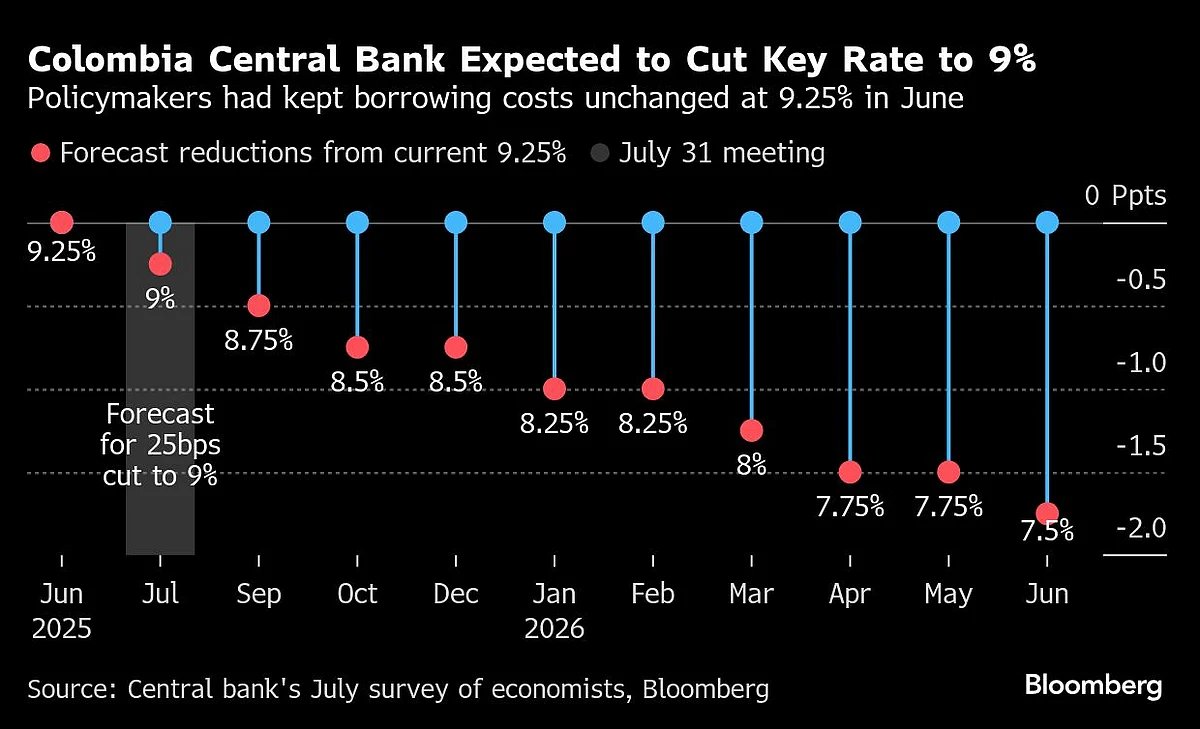

Elsewhere, central bankers in Japan and Brazil are also likely to keep rates unchanged, while cuts are anticipated in South Africa, Chile, Ghana, Pakistan and Colombia. Investors will also watch for new International Monetary Fund’s forecasts, global purchasing manager index readings, and a barrage of GDP and inflation data in Europe.

Asia

Asia’s central bank highlight comes Thursday, with the Bank of Japan expected to hold its benchmark rate steady at 0.5%. Governor Kazuo Ueda’s reaction to the US trade deal will be a focus after his deputy said the agreement boosted the likelihood of economic forecasts being met — a key condition for another rate hike.

A slew of data will reflect the impact of Trump’s tariff campaign. Trade figures are due from the Philippines, Hong Kong, Sri Lanka, Thailand, South Korea and Indonesia, while manufacturing PMI figures are due across the region.

China gets two sets of July PMI data at the end of the week, with attention on whether the official gauge can edge higher for a third month and S&P Global’s index can stay in the expansion zone. Others releasing PMI statistics include Indonesia, South Korea, Malaysia, the Philippines, Thailand, Taiwan and Vietnam, all on Friday.

Meantime, Australia gets second quarter data that’s expected to show consumer inflation cooled a tad, which could give the Reserve Bank room to resume its rate cutting cycle when it next sets policy on Aug. 12.

Pakistan’s central bank may cut rates on Wednesday, two days before the country — and Indonesia — gets new inflation readings.

-

For more, read Bloomberg Economics’ full Week Ahead for Asia

Europe, Middle East, Africa

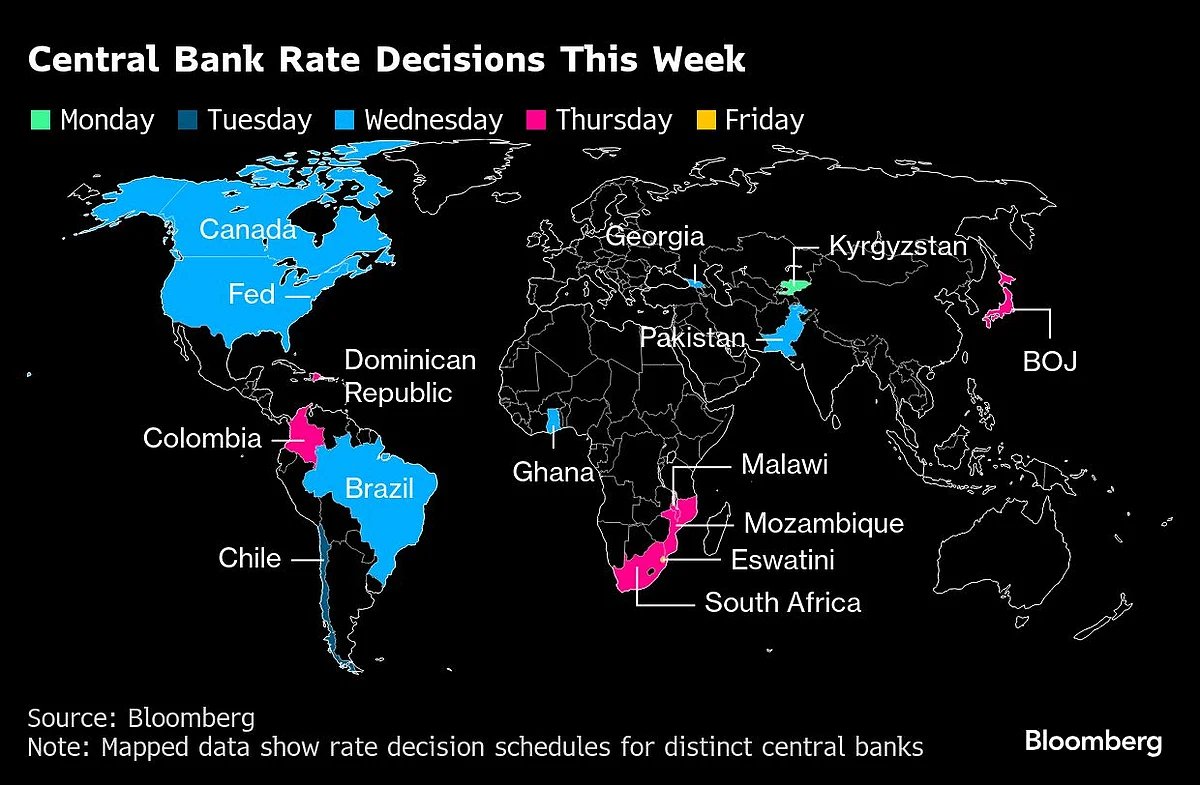

Output and inflation data across Europe takes center stage. Economists in a Bloomberg poll expect Wednesday’s figures to show euro-area GDP remained flat in the three months through June, after a 0.6% expansion in the first quarter. That performance was lifted by a frontloading in trade before Trump’s expected announcement of global import duties.

Among the bloc’s biggest economies, Germany is forecast to see the worst performance, with output slipping 0.1% from the previous quarter. Spain is expected to keep growing by 0.6%, with France and Italy expanding just slightly. Smaller economies publish their numbers throughout the week, with Ireland — so often a wild card for the bloc’s economy — kicking things off on Monday.

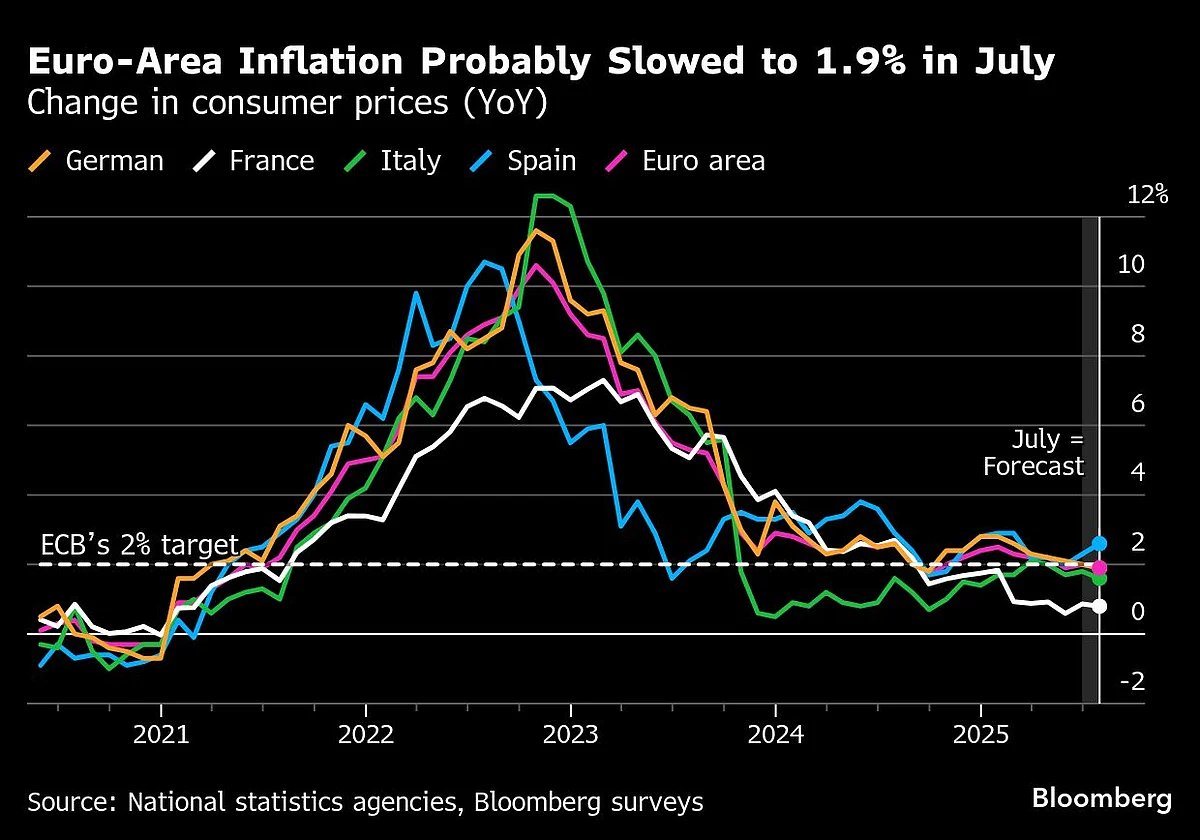

Meanwhile, inflation data for the euro area on Friday are set to confirm the European Central Bank’s confidence that it’s been brought under control. Consumer prices are forecast to have risen 1.9% in July, less than the previous month’s 2% and just below the central bank’s goal. A measure of underlying inflation probably remained steady, at 2.3%.

With most of Europe in vacation mode, only a single ECB speaker has a scheduled appearance — Spain’s José Luis Escrivá, on Monday — while results from the central bank’s monthly survey of consumers’ inflation expectations are due a day later, and its wage tracker comes on Wednesday.

The Bank of England goes into a quiet period ahead of its Aug. 7 rate decision, with economic releases on the UK agenda primarily linked to housing.

-

For more, read Bloomberg Economics’ full Week Ahead for EMEA

Rate decisions are scheduled across Africa:

-

A steep slowdown in inflation will likely see officials in Ghana lower borrowing costs by 250 basis points to 25.5% on Wednesday. Its real rate is the highest it’s been since at least 2005, providing room for the central bank to deliver the biggest reduction in more than two decades.

-

South Africa is set to extend its longest easing cycle since 2019 as inflation is anticipated to remain benign. Economists surveyed by Bloomberg expect the central bank to cut on Thursday by 25 basis points, to 7%.

-

On the same day, Malawi’s policymakers are poised to leave their key rate unchanged at 26% due to foreign-exchange constraints and persistent price pressures.

-

A technical recession in Mozambique will probably convince policymakers to opt for further easing on Thursday to stimulate the economy. It has cut by 625 basis points since January 2024.

-

Eswatini, whose currency is pegged to the rand, will probably lower its benchmark by a quarter point on Friday, to 6.5%.

Latin America

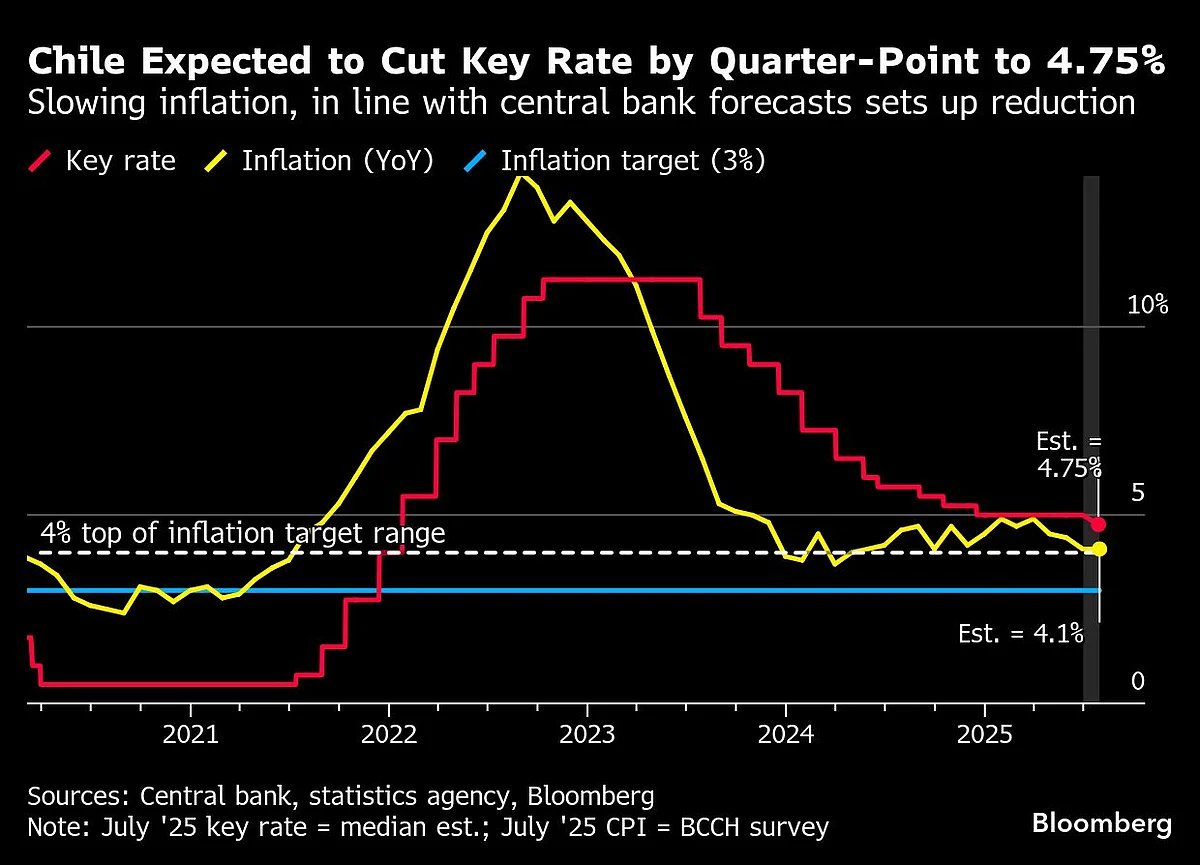

Chile’s central bank on Tuesday is likely to deliver its first rate cut of 2025, opting for a quarter-point reduction to 4.75%.

Consumer prices last month cooled more than expected and inflation is once again slowing in line with central bank forecasts, which have the headline reading back to the 3% target in 2026.

Mexico’s flash second-quarter data posted on Wednesday should show Latin America’s No. 2 economy posting slight quarterly and year-on-year expansions amid the drag from Trump’s trade and tariff policies.

Most analysts see the second half of the year posing a greater challenge.

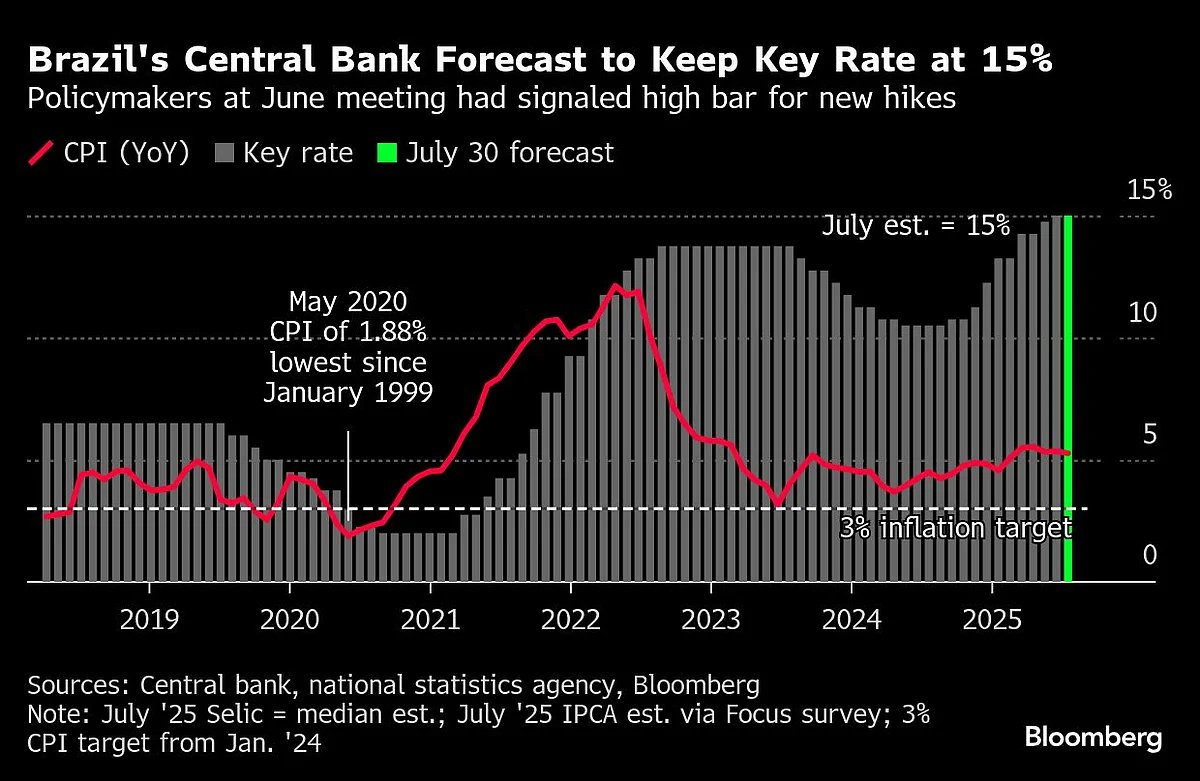

In the region’s second central bank rate decision of the week, Banco Central do Brasil is widely expected to draw a line under a seven-meeting, 450 basis-point tightening campaign and keep the key Selic rate at 15%.

Mexico’s flash second-quarter data posted on Wednesday should show Latin America’s No. 2 economy posting slight quarterly and year-on-year expansions amid the drag from Trump’s trade and tariff policies.

Most analysts see the second half of the year posing a greater challenge.

In the region’s second central bank rate decision of the week, Banco Central do Brasil is widely expected to draw a line under a seven-meeting, 450 basis-point tightening campaign and keep the key Selic rate at 15%.

Peru on Friday kicks off consumer price reports for the region’s big inflation targeting economies. The early consensus among economists is that July’s annual reading will come in near June’s 1.69% print.

. Read more on Global Economics by NDTV Profit.