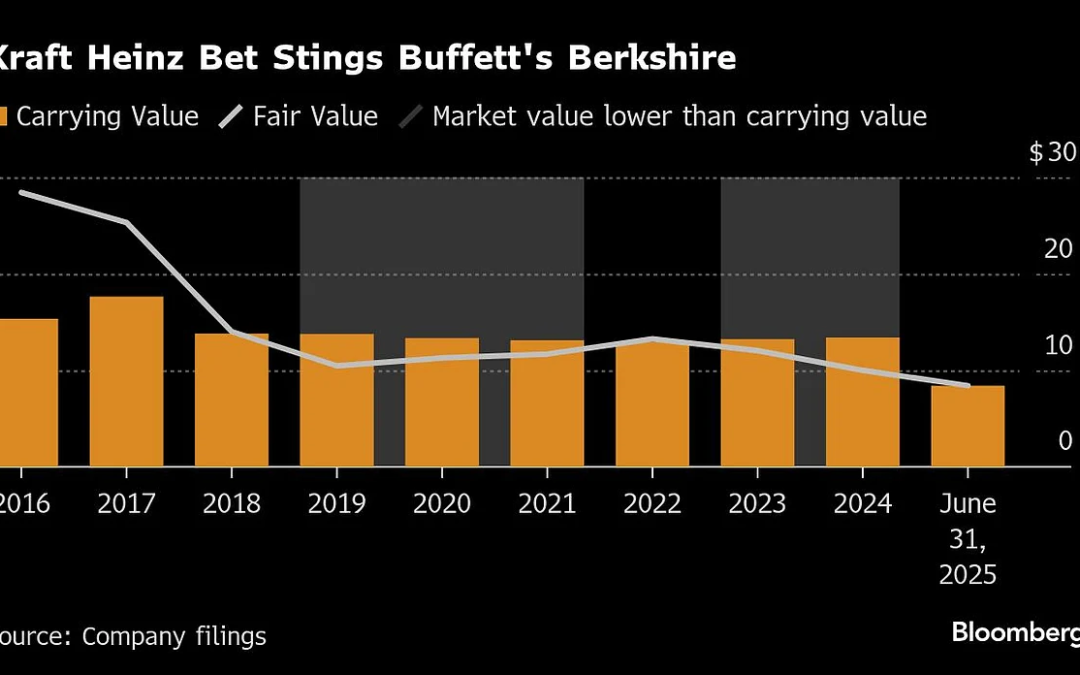

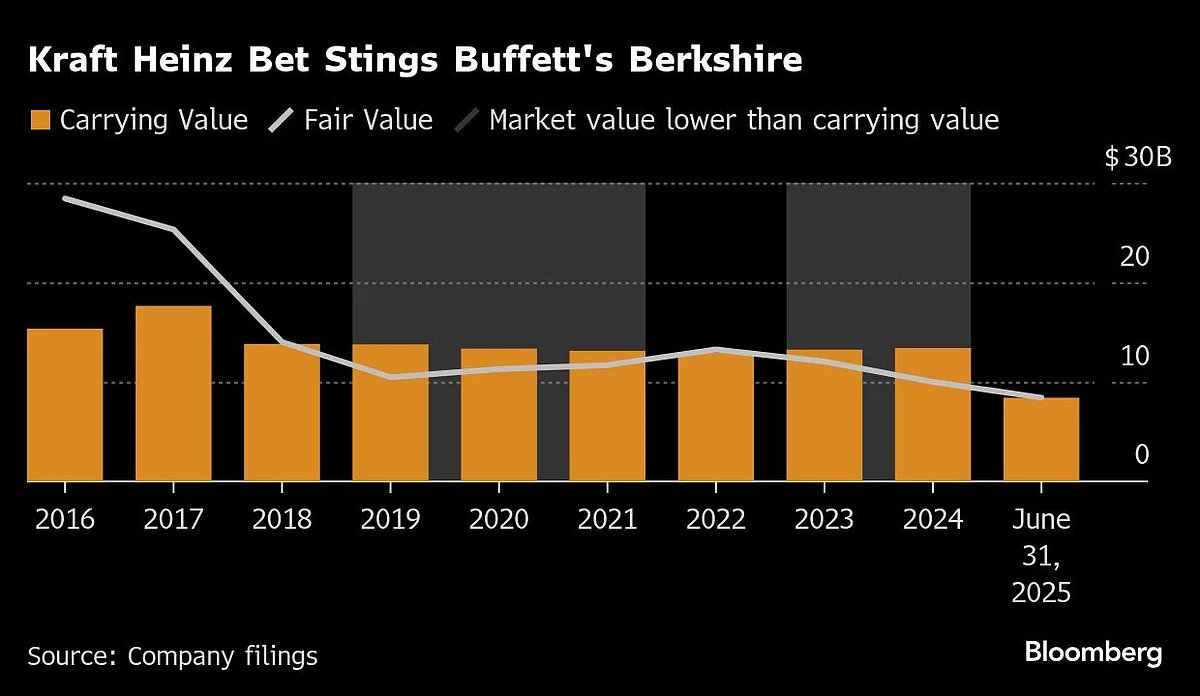

Warren Buffett’s Berkshire Hathaway Inc. took a $3.8 billion impairment on its Kraft Heinz Co. stake, the latest hit to a bet that’s weighed on the billionaire investor’s company in recent years.

On Saturday, Berkshire marked down the carrying value of its Kraft Heinz investment to $8.4 billion, down from more than $17 billion at the end of 2017. It’s a rare disappointment for Buffett, 94, who was an instrumental force in the merger of both Kraft and Heinz about a decade ago.

While the billionaire is still in the black on his bet, the stock of the packaged foods giant has fallen 62% since then. During the same period, the S&P 500 has risen 202%. Berkshire’s Kraft Heinz stake is now marked at its fair value as of the end of June.

The writedown was “overdue,” said Kyle Sanders, an analyst at Edward Jones. “You could argue they should have done it a couple of years ago.”

Kraft Heinz is now contemplating a spinoff of part of its business as it grapples with headwinds including inflation weighing on consumers’ spending and people seeking healthier alternatives to its products. Last month, the company posted a decline in sales that wasn’t as bad as analysts had predicted, in part thanks to higher prices.

In recent months, Berkshire has signaled that it’s taking a slight step back with its ties to Kraft Heinz. In May, Kraft Heinz announced that Berkshire gave up seats on the packaged foods company’s board. And because Buffett’s company is now limited to what Kraft Heinz discloses publicly, Berkshire said it would start reporting its share of Kraft Heinz’s earnings on a one-quarter lag.

The writedown, disclosed Saturday in a regulatory filing, was driven in part by the sustained decline in fair value. But the company also said it considered its relinquishing of those board seats and Kraft Heinz’s push to evaluate strategic transactions when determining how much of a charge to take.

“Given these factors, as well as prevailing economic and other uncertainties, we concluded that the unrealized loss, represented by the difference between the carrying value of our investment and its fair value, was other-than-temporary,” Berkshire said in the filing.

While Buffett’s conglomerate said it owns 27.4% of Kraft Heinz stock at the end of June, the writedown could ease the path to a reduction of that holding in the future, according to Edward Jones’s Sanders.

“I think they’re giving themselves more flexibility to potentially exit their position in the future,” he said. “This is one of Warren’s largest missteps in the past couple of decades. It might just be time to move on from it.”

Cash Hoard

Buffett’s cash pile ended up dropping 1% in the three months through June, to $344 billion, the first time in three years that the war chest has shrunk. Those funds had previously kept soaring to all-time highs as Buffett struggled to find opportunities to invest.

What Bloomberg Intelligence Says

“Berkshire Hathaway is facing headwinds from US trade policies, lower interest rates and revisions to federal energy tax policy, but capital generation should remain strong from its inelastic demand businesses.”

— Senior Industry Analyst Matthew Palazola and Senior Associate Analyst Eric Bedell

Buffett ended up taking a cautious approach to the stock market in the second quarter. He was a net seller of other companies’ shares during the period, offloading about $3 billion of equities.

He even steered clear of Berkshire’s own stock, forgoing any buybacks. He’s been on the sidelines for repurchases for roughly a year now, despite the stock falling 12% after Buffett announced in May that he would step down as chief executive officer at the end of the year.

Buffett’s perceived cautious stance toward the market, including his own stock, may weigh on Berkshire’s share performance compared with the market, according to Sanders.

“The things that they need to do to get the stock working, they’re just not willing to pull the trigger on yet,” he said.

Operating Profit

Berkshire had a weaker second quarter at its operating businesses. Profit dropped 3.8% to $11.16 billion, driven by a decline in underwriting earnings at its insurers.

Its auto insurer, Geico, posted pretax underwriting earnings that rose 2% to $1.8 billion in the second quarter. The unit’s underwriting expenses surged 40% in the period, as the company spent more to increase its policy count.

“They were behind their peers, they lost market share and it took a couple of years to turn the ship,” Sanders said. “That comeback is finally on solid footing.”

Tariffs have weighed on some of Berkshire’s businesses. This year through the end of June, revenues at some consumer companies including Fruit of the Loom and Garan, known for its Garanimals children’s products, were down in part because of business restructuring and the uncertainty of the trade war.

Berkshire cautioned that geopolitical and macroeconomic issues may weigh on its results.

“The pace of changes in these events, including tensions from developing international trade policies and tariffs, accelerated through the first six months of 2025,” the company said in the filing.

Energy, Railroad

Berkshire’s utility business, which runs Pacificorp, MidAmerican and NV Energy, posted a 7% increase in operating earnings. The company said it is currently evaluating the impact of President Donald Trump’s tax law as it accelerates the phase-out of clean energy production.

At its railroad, BNSF, operating earnings rose 19% to about $1.5 billion, an increase Berkshire attributes to increased productivity and a lower tax rate. The unit, which Berkshire acquired in 2010, has been caught up in dealmaking speculation in recent weeks. Two major competitors, Union Pacific Corp. and Norfolk Southern Corp., struck a $72 billion deal to create the first transcontinental railroad operator.

BNSF’s strong performance in the second quarter calls into question the necessity for the railroad to do its own deal to remain relevant, according to Cathy Seifert, an analyst at CFRA Research.

“We just came out of a quarter where they’ve had to write down a deal that didn’t work out very well,” she said. “So there’s really a hesitancy to pay up when you’ve got a potential target that’s been bid up in anticipation of you making a deal.”

. Read more on Business by NDTV Profit.