Indonesia’s luxury hotel sector is experiencing a transformation unlike anything seen in Southeast Asia. From the crystalline waters of Bali to the emerging cultural epicenter of Nusantara, the archipelago’s premium hospitality landscape is expanding at a pace that even industry veterans find remarkable. But what exactly is fueling this five-star revolution across 17,000 islands?

The answer isn’t simple – and that’s precisely what makes it fascinating. Behind every gleaming resort facade and infinity pool lies a complex web of economic shifts, cultural evolution, and strategic governmental vision that’s reshaping how the world experiences Indonesian luxury.

The Numbers Tell a Compelling Story

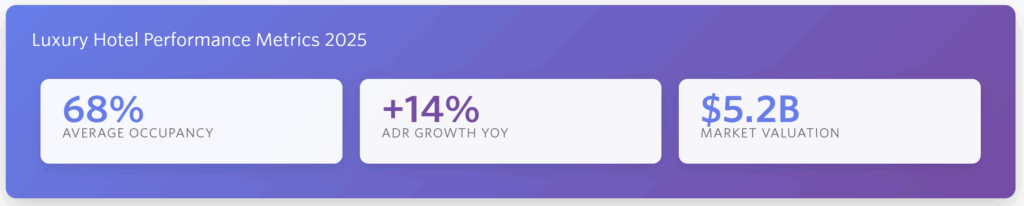

Indonesia’s luxury hospitality market reached a valuation of approximately USD 5.2 billion in 2025, marking a significant acceleration from previous years. The upscale segment is projected to grow at a compound annual growth rate of 1.7%, while the luxury segment follows closely at 1.3% through 2029. These figures represent more than statistical growth – they reflect a fundamental shift in how Indonesia positions itself on the global tourism stage.

International visitor arrivals tell an equally compelling narrative. From January through May 2025, Indonesia welcomed 5.44 million international tourists, marking a 3.8% year-on-year increase. More importantly, international visitor spend is on track to reach IDR 344 trillion this year – nearly 12% above the previous record set in 2019.

According to data from Hotels-Scanner, luxury properties across major Indonesian destinations have seen average occupancy rates climb to 68% in 2025, with average daily rates increasing by 14% compared to 2024.

Beyond Bali – Destination Diversification

While Bali continues to anchor Indonesia’s luxury tourism narrative, the archipelago’s hospitality expansion tells a more nuanced story. The government’s strategic pivot from the ambitious “Ten New Bali Project” to the more focused “Five Super Priority Destinations” represents a calculated approach to sustainable luxury development.

Lake Toba in North Sumatra has emerged as a serene alternative to beach-centric luxury, attracting high-end wellness retreats and eco-resorts. Borobudur Temple in Central Java draws affluent cultural tourists seeking authentic heritage experiences wrapped in contemporary comfort. Mandalika in West Nusa Tenggara is positioning itself as a premium beach destination with world-class infrastructure,while Labuan Bajo in East Nusa Tenggara serves as the gateway to Komodo National Park , appealing to adventure-luxury travelers.

Likupang in North Sulawesi rounds out this quintet, offering pristine diving sites and untouched natural beauty that resonates with luxury travelers seeking exclusivity. Each destination brings distinct characteristics that collectively broaden Indonesia’s luxury appeal beyond the saturated Bali market.

The Nusantara Effect

Perhaps nothing symbolizes Indonesia’s luxury hospitality ambitions more dramatically than Nusantara – the USD 33 billion capital city project rising from the forests of East Kalimantan. This isn’t merely administrative relocation; it’s a statement of intent that reverberates through the entire hospitality sector.

The project has already catalyzed luxury hotel development in previously overlooked regions. East Kalimantan’s hotel supply has grown at a compound annual rate of 4.2% since planning began , though it still represents only 2.3% of Indonesia’s total classified hotel inventory. International hotel brands are positioning themselves early, recognizing that Nusantara will create demand for premium business travel accommodations and high-end diplomatic hospitality.

The ripple effects extend far beyond the immediate construction zone. Infrastructure improvements – new airports, highways, and digital connectivity – are opening previously inaccessible areas to luxury development. What was once considered remote is becoming reachable, and reachability is the first prerequisite for luxury hospitality investment.

The Demographics of Desire

Indonesia’s expanding middle class isn’t just an economic statistic – it’s a fundamental driver reshaping the luxury hospitality landscape from within. The country’s middle-class consumption has grown at approximately 12% annually over recent years, and projections indicate Indonesia will become the world’s fourth-largest consumer market by 2030, surpassing established economies.

This demographic shift creates a fascinating dynamic. Affluent Indonesians are increasingly seeking premium domestic travel experiences, reducing the sector’s historical dependence on international arrivals. They expect world-class amenities, sophisticated dining, and Instagram-worthy aesthetics – standards that push properties to maintain competitive luxury positioning.

- Domestic luxury travelers now account for approximately 42% of upscale hotel bookings across major Indonesian destinations

- Weekend occupancy at luxury resorts has increased by 23% year-on-year , driven primarily by domestic demand

- Indonesian guests show particular preference for integrated resorts offering multiple dining and entertainment options within the property

- The average spend per stay for domestic luxury travelers has increased by 18% in 2025 compared to 2024

- Multigenerational family travel among affluent Indonesians is creating demand for villa-style accommodations and family-oriented luxury experiences

This domestic demand provides crucial stability. While international tourism fluctuates with global economic conditions, geopolitical tensions, or pandemic-related disruptions, domestic luxury travel offers resilience that makes hotel investments more attractive to institutional capital.

International Capital Flows

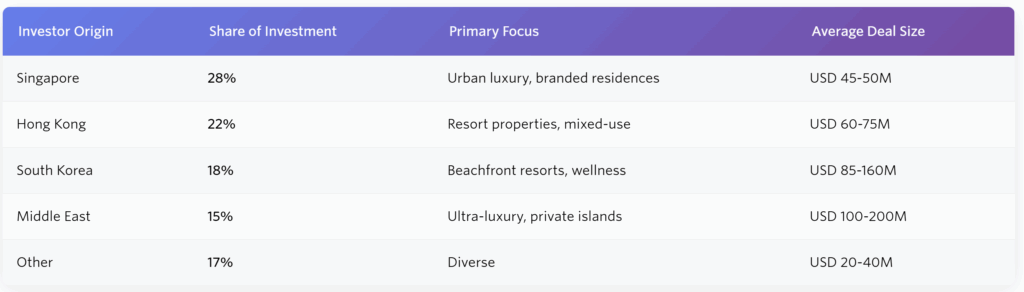

Foreign investment in Indonesia’s luxury hotel sector reached approximately USD 218 million in 2025, with transactions concentrated in the upscale to luxury segments. The investment profile reveals interesting patterns about who’s betting on Indonesian luxury hospitality and why.

Foreign buyers contribute to approximately 64% of luxury hotel investment volume, attracted by Indonesia’s favorable foreign ownership regulations for hotels rated two stars and above. The regulatory framework allows 100% foreign ownership through a PMA structure, making Indonesia considerably more accessible than some regional competitors with stricter foreign investment limitations.

Notable transactions underscore this trend. The Sofitel Bali Nusa Dua changed hands for USD 160 million to South Korean investors in a deal that signaled confidence in Bali’s enduring appeal. The Pullman Jakarta Central Park sold for USD 73 million to Hong Kong-based Melrose Park Developments, attracted by the property’s proven cash flow generation even during pandemic disruptions. These aren’t speculative plays – they’re calculated investments backed by rigorous underwriting and long-term market conviction.

The Visa Revolution

Indonesia’s evolving visa policies represent strategic tools in the luxury hospitality growth equation. The golden visa program, introduced in July 2024, targets high-net-worth individuals, offering five or ten-year residency permits to those making substantial investments . This isn’t just about immigration policy – it’s about creating a class of affluent long-term residents who will utilize luxury accommodations for extended periods.

The extension of visa-free travel to citizens from additional countries creates complementary effects. The Indonesian Tourism Ministry projects these visa liberalizations could generate approximately USD 42 billion for the national tourism sector through 2026. For luxury hotels, visa-free access reduces friction in the booking decision process, particularly for spontaneous high-value travelers who might otherwise choose destinations with simpler entry requirements.

These policy shifts work synergistically. Golden visa holders establish bases in Indonesia, bringing family and business associates who book luxury accommodations. Visa-free tourists discover the archipelago’s offerings, with a percentage converting to repeat visitors or even golden visa applicants. The virtuous cycle amplifies luxury hotel demand from multiple angles simultaneously.

Source Market Dynamics

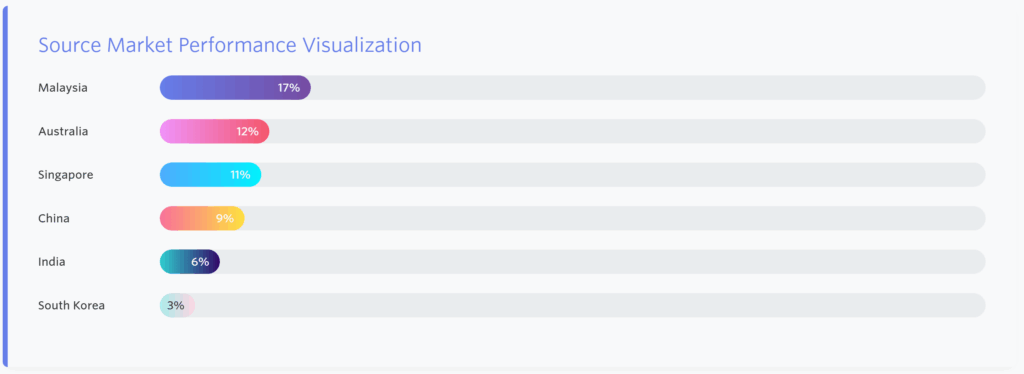

The composition of international visitors to Indonesia reveals shifting patterns that luxury hoteliers are racing to understand and exploit. Malaysia leads source markets with 17% of arrivals, followed by Australia at 12% and Singapore at 11%. However, the story behind these numbers is more complex than simple rankings suggest.

Australian visitors have exceeded their 2019 visitation levels by approximately 3%, with 1.4 million trips to Indonesia in 2024. This market demonstrates particular affinity for Bali’s luxury offerings, with Australian guests showing higher average spending per stay compared to other source markets. Their proximity, currency strength, and cultural familiarity make them ideal luxury hotel guests.

China’s slower recovery – currently at only 38% of 2019 levels – reflects broader regional patterns tied to economic headwinds and Yuan weakness. However, South Korea has emerged as a growth story, exceeding 2019 levels and climbing in market share rankings. Korean travelers demonstrate strong interest in wellness-oriented luxury properties and Instagram-aesthetic resorts, driving development tailored to these preferences.

India’s growing presence at 6% of arrivals represents an emerging opportunity. As India’s affluent class expands, Indonesian luxury hoteliers are adapting offerings to appeal to Indian preferences – vegetarian cuisine options, family-oriented facilities , and culturally sensitive service approaches that make Indian guests feel genuinely welcomed rather than merely accommodated.

Infrastructure as Enabler

You can’t build luxury hotel empires on inadequate infrastructure. Indonesia recognizes this fundamental truth, and the government’s infrastructure push is perhaps the most underappreciated driver of luxury hospitality growth.

Air connectivity has expanded significantly. Total air passenger numbers reached 78.3 million in 2024, representing 79% of 2019 levels, with international passenger recovery actually outpacing domestic recovery. New routes connect previously underserved luxury destinations directly to major source markets, eliminating the friction of multiple connections that deterred high-end travelers.

But it’s not just about airports. Road networks linking resorts to cultural attractions allow luxury properties to position themselves as gateways to authentic experiences rather than isolated beach compounds. Digital infrastructure enables the seamless connectivity that modern luxury travelers consider non-negotiable – high-speed internet isn’t an amenity anymore; it’s a baseline expectation.

The Nusantara capital project exemplifies infrastructure’s catalytic role. Beyond the immediate construction, the project is driving port improvements, telecommunications upgrades, and transportation modernization throughout Kalimantan. These enhancements make luxury hotel development viable in areas that were previously logistically challenging and economically questionable.

Brand Positioning and Market Segmentation

International luxury brands are approaching Indonesia with sophisticated segmentation strategies that recognize the archipelago’s diversity. Aman Resorts emphasizes ultra-exclusivity and cultural immersion in heritage locations. Four Seasons focuses on transformative travel experiences with impeccable service standards. Ritz-Carlton positions urban luxury as sophisticated urbanity, while their Reserve properties offer intimate, bespoke resort experiences.

- Ultra-luxury brands (Aman, Six Senses, Rosewood) target guests seeking transformative wellness experiences and cultural authenticity, with average room rates exceeding USD 800 per night

- Premium luxury chains (Four Seasons, Ritz-Carlton, Mandarin Oriental) balance sophisticated amenities with broader accessibility, capturing business luxury travelers and affluent leisure guests

- Upper-upscale brands (Pullman, Sofitel, Marriott Luxury Collection) offer contemporary luxury at moderate price premiums, appealing to aspirational domestic travelers and international tourists seeking recognized quality

- Boutique independents differentiate through hyper-local design, intimate scale, and personalized experiences that larger brands struggle to replicate authentically

- Branded residences are emerging as a hybrid category, blending hotel services with ownership opportunities for high-net-worth individuals seeking Indonesian property investments

This segmentation creates a luxury ecosystem where properties compete not just on amenities but on clearly defined value propositions. A guest choosing between Aman and Four Seasons isn’t simply comparing pools and restaurants – they’re selecting fundamentally different luxury philosophies.

Sustainability as Competitive Advantage

Sustainability has evolved from marketing buzzword to operational imperative in Indonesia’s luxury hotel sector. Apurva Kempinski Bali gained international recognition for sustainable practices in early 2025, setting benchmarks that competitors are scrambling to meet. But this isn’t altruism – it’s business strategy grounded in guest expectations and operational efficiency.

Affluent travelers increasingly evaluate accommodations through environmental and social impact lenses. Properties demonstrating genuine commitment to sustainability – not greenwashing – attract guests willing to pay premiums for alignment with their values. This creates competitive moats that are difficult for laggards to overcome quickly.

Operationally, sustainable practices reduce costs. Solar installations decrease energy expenses in a country with abundant sunshine. Water recycling systems lower utility costs and enhance resilience during dry seasons. Locally sourced food reduces transportation costs while supporting community relationships that provide intangible benefits when challenges arise.

The Indonesian government’s emphasis on sustainable tourism development in the Five Super Priority Destinations reinforces this trend. Properties incorporating sustainability from the design phase gain approval advantages and access to international development financing often conditional on environmental standards. Retrofitting sustainability is expensive; building it in from inception is strategic.

Technology Integration

Indonesia’s luxury hotels are leveraging technology to enhance personalization without sacrificing the human touch that defines premium hospitality. Digital check-in reduces arrival friction while freeing staff to focus on genuine welcome experiences. AI-powered preference tracking enables anticipatory service that feels intuitive rather than intrusive.

Mobile apps allow guests to control room environments, request services, and access property information without language barriers that might create awkwardness. Virtual concierge services provide 24/7 assistance for basic needs, reserving human concierges for complex requests where expertise and relationship add genuine value.

Behind the scenes, revenue management systems optimize pricing dynamically based on demand patterns, competitive positioning, and guest segment value. These systems enable luxury properties to maximize revenue while maintaining rate integrity that preserves brand positioning – a delicate balance that manual approaches struggle to achieve consistently.

Contactless payment systems, digital keys, and automated amenity delivery don’t reduce luxury – they eliminate mundane friction points that detract from the immersive experiences guests seek. Technology succeeds when it becomes invisible infrastructure supporting memorable human interactions, not when it replaces those interactions entirely.

The Branded Residence Phenomenon

Branded residences represent a fascinating evolution in Indonesia’s luxury hospitality landscape, blurring lines between hotels and real estate. These properties offer fractional ownership or full-title units managed by luxury hotel brands, providing services and amenities comparable to hotel experiences while offering ownership equity that traditional hotel stays cannot.

For developers, branded residences offer compelling economics. Unit sales provide upfront capital that reduces development risk compared to traditional hotel financing. Buyer deposits fund construction, while the hotel brand provides operational expertise, booking systems, and marketing reach that independent developers lack.

For buyers – predominantly high-net-worth Indonesians and regional investors – branded residences offer personal use flexibility combined with income generation during non-use periods. The hotel brand manages rentals, maintaining service standards while providing owners with hassle-free returns. Golden visa eligibility for property investors creates additional appeal for foreigners considering Indonesian residence.

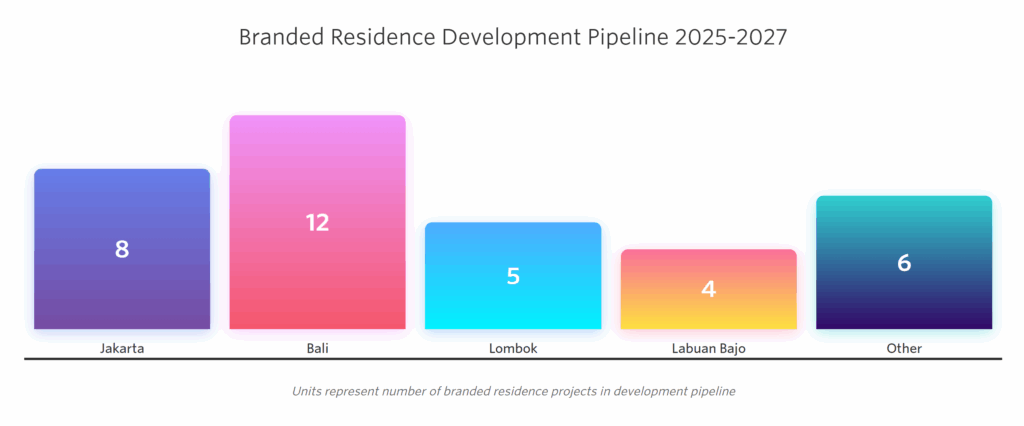

Bali leads branded residence development with 12 projects in the pipeline through 2027, followed by Jakarta with eight projects. These developments cluster in established luxury markets where brand recognition carries maximum value and buyer confidence is highest. However, emerging destinations like Lombok and Labuan Bajo are beginning to attract branded residence interest as infrastructure improvements reduce perceived risk.

Challenges Beneath the Surface

Despite robust growth trajectories, Indonesia’s luxury hotel sector faces challenges that temper unbridled optimism. Land availability in established markets like Bali has become increasingly constrained, driving prices to levels that challenge development economics. Local regulations limiting new hotel construction in certain areas aim to prevent overdevelopment but also restrict supply growth that might otherwise occur.

Skilled labor shortages present ongoing challenges. Luxury hospitality requires sophisticated service capabilities that take years to develop. While Indonesia has strong hospitality education infrastructure, competition for top talent is intense. Properties in emerging destinations struggle particularly to attract experienced managers willing to relocate from established markets like Bali or Jakarta.

Currency volatility creates complexity for international investors. The Indonesian Rupiah’s fluctuations against major currencies introduce foreign exchange risk that must be hedged or accepted. Properties generating revenues in Rupiah while servicing USD-denominated debt face particular exposure when currency movements are adverse.

Regulatory complexity – while improving – remains more challenging than in some competing Southeast Asian destinations. Foreign ownership structures through PMA entities add layers of compliance compared to more direct ownership models available elsewhere. Land title systems, particularly HGB renewals, introduce uncertainties that sophisticated investors price into their underwriting but that nonetheless create friction.

The Long View Forward

Indonesia’s luxury hotel growth isn’t a temporary boom driven by post-pandemic revenge travel or speculative capital chasing yields. It’s a structural shift grounded in demographic evolution , strategic government vision, infrastructure investment, and Indonesia’s inherent appeal as a diverse, culturally rich, naturally stunning destination that has been underutilized relative to its potential.

The projection that Indonesia will become the world’s fourth-largest consumer market by 2030 ensures domestic luxury demand will continue strengthening. International arrivals have room for substantial growth – Indonesia receives far fewer tourists per capita than Thailand despite comparable attractions. As infrastructure improves and destination diversity expands beyond Bali’s dominance, that gap will narrow.

The challenge for luxury hoteliers isn’t whether demand will materialize – it’s how to position properties to capture that demand profitably while maintaining the service standards and experiential quality that justify premium pricing. Success will require sophisticated understanding of segmented guest preferences, operational excellence that balances technology with human touch, and strategic positioning that differentiates each property in an increasingly competitive landscape.

What’s driving luxury hotel growth across Indonesia? It’s not one factor but a convergence – economic expansion meeting governmental vision, infrastructure enabling accessibility, demographic shifts creating domestic demand, and Indonesia’s inherent appeal finally receiving the hospitality infrastructure worthy of its potential. The archipelago isn’t becoming the next Bali. It’s becoming the first Indonesia – and that’s a far more interesting story.

The post What’s Driving Luxury Hotel Growth Across Indonesia appeared first on Trade Brains Features.